There are a number of tests for determining whether a warrant is worth buying.

Theoretical value

When an investor buys a warrant instead of the underlying stock, at that point he saves the difference between the stock price and the warrant price (also called the premium of a warrant).

If, for example, the underlying share costs $6 and the warrant costs $4, he saves $2. The lower the warrant price, then the greater the savings. The investor can do whatever he wishes with the money he saves.

For example, he can deposit the money in a savings account, and receive interest.

The warrant’s theoretical value is the amount saved, plus the interest on that amount.

Assuming that the underlying stock price stays the same.

In that case, an investor should buy a warrant only if it is priced at or below its theoretical value. When an investor buys a warrant at its theoretical price, he is spending the same amount of money for the underlying stock that he would have paid for the stock directly on the stock market.

Technically, every investor has his own theoretical price, which depends on the interest rate available to him.

In order to simplify things for most investors, however, theoretical prices are calculated according to the common interest rate that is available.

The following formula is used to calculate the theoretical value of a warrant:

![]()

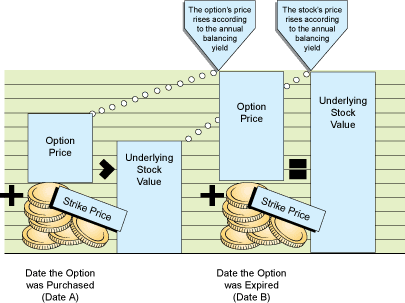

Annual balance yield

The annual balance yield is the percentage that both the stock and warrant prices must increase during the period between the purchase of the warrant and the date on which it is exercised in order for the exercise price plus the warrant price to equal the price of the underlying stock.

If, for example, the annual balance yield is 20%, then both the stock and warrant prices must rise 20% per year. If the underlying stock price rises by less than the annual balance yield, then the increase in the warrant price will rise even less. In this case, the buyers of the warrant will earn less money than those who purchased the stock directly. However, if the stock price rises by more than the annual balance yield, then the warrant price will increase even faster. Under these conditions, buying the warrant is more profitable than buying the underlying stock.

Immediate exercise premium

The immediate exercise premium represents the loss or gain that an investor earns by buying a warrant and exercising it immediately, as opposed to buying the underlying stock directly. This value is measured as a percentage of the underlying stock price, and it is calculated using the following formula:

![]()

In the example of the American Bio Medica warrant, the immediate exercise premium is 28.9%. This means that an investor who bought the warrant and exercised it immediately spent 28.9% more than an investor who bought the stock at its market price. However, if the value is negative, then purchasers of warrants pay less than investors who buy the underlying stock directly.

Clearly, if the value is positive, no investor will buy the warrant in order to exercise it immediately. Investors who buy the option expect the underlying stock price to rise by more than the annual balance yield. They will then make more money than they would have made by buying the stock itself.

Normally, a warrant with a negative immediate exercise premium is not sold at all. If such a warrant were sold, investors in the market would buy it, exercise it, sell the stock, and earn an immediate profit. This would continue until the warrant price rose, the stock price fell, and the immediate exercise value reached zero.

These reasons explain why warrants and options nearly always sell at prices that are higher than their immediate exercise values.

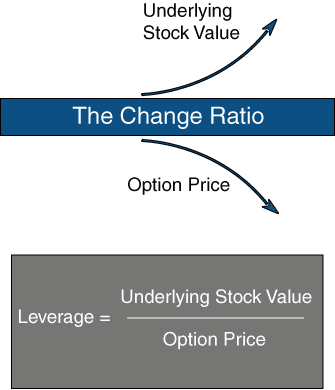

Leverage

Warrants and most options cost less than their underlying assets. This power over assets using less money than the assets are worth is called “leverage.” Leverage is calculated by dividing the value of the underlying asset by the value of the options. For example, a $2 warrant on a $16 stock has a leverage of 8.

The change ratio (also called “delta”) indicates how much the price of a warrant can be expected to change when the underlying stock price changes by 1%. A warrant that experiences a 6% increase in stock price when the underlying stock increases by 2% has a change ratio of 3. This warrant would drop 3% in value for a 1% decrease in stock price.

The change ratio is only an approximate guide. And, since both securities are traded independently, it is possible for the stock to go up 1% while the warrant value falls!

![]()